The Government of Mexico has repeatedly mentioned that one of its main goals in the National Hydrocarbons Plan is the production of 2.6 million barrels of crude oil per day at the end of 2024.

The production profile brings components such as the base production already in place of oil fields operating in the country, the plan proposes operations of drilling and development of more than 20 new fields of which PEMEX has already been hiring and asking for authorizations for the development, contains projects related to secondary and improved recovery of the deposits that already exist and production that is associating future discoveries.

PEMEX has 22 fields for new development, of which 18 are in shallow waters.

Thanks to the investment that is planned for drilling and infrastructure, there is the possibility that in these 18 fields we might find more extension and thickness in their deposits to be found, since this has happened before.

The energy policy is being modified by the nature of the political change in the Country, the strengthening of PEMEX could be increased with support of the process of migration of Oil Assignments (Farmouts).

Fracking is a technique that is required to obtain physical resources, in the United States the increase in production is known derived from the use of this technique. Thanks to it, a high production of liquids and gas is obtained which are offered at a low price to countries like Mexico. Fracking in Mexico is a prospective resource since, whether or not it can be used as a production technique depends of a previous exploration in order to know if it can be extracted profitably since the operation in Mexico might be more expensive.

Using all the tools provided by the current legal framework in Mexico regarding energy is essential for PEMEX to increase its technical execution and financial capacity in such a way that it shares the risk.

Successful decisions will give more opportunities for the development not only of the sector, but also of the human component that makes it possible, such as engineers, people who have service companies, investors, among others.

If you want to know more information about experts from the Energy Sector in Mexico, click on the video to see the interview of Gaspar Franco Former Commissioner of the CNH and Graciela Álvarez Hoth, General Director of NRGI Broker.

Check out our news section and follow us on our social media networks.

https://nrgibroker.com/wp-content/uploads/2019/08/portadas-mailchimp.png10001000Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2019-08-12 22:25:542019-08-21 10:02:48Fundamental factors to strengthen Pemex

As new offshore operators continue to settle into their awarded blocks and develop them into a stable production phase as quickly as possible, new models of collaboration between the public and private sectors must arise in view of the new administration’s focus on PEMEX, panelists at the Mexico Oil & Gas Summit 2019, said on Wednesday July 17 in Mexico City.

Private operators and service providers are ready to comply with government plans: Graciela Alvarez Hoth, panel moderator

According to Graciela Álvarez Hoth, CEO of NRGI Broker, both private operators and Mexican service providers are ready to collaborate with the government’s plans to strengthen the NOC while also building upon the many successes achieved in a short period of time within the fields awarded through the bidding rounds. “The number of new discoveries highlights the need for exploration activities to capitalize on the available opportunities in the country,” she said.

Álvarez Hoth made her remarks on the first day of the two-day summit held at the Sheraton Maria Isabel Hotel as part of her introductory remarks to the panel she moderated, entitled “Offshore Project Development: The Road to First Oil.”

Four panelists from key public and private institutions provided a crucial mix of perspectives on Mexico’s offshore development, particularly in terms of achieving production in new shallow water fields.

“Talos Energy wants to have a positive impact in Mexico. The president has set his production goal and our goal is to do our part to help. ”

Francisco Noyola, Country Manager of Mexico for Talos Energy, was the first to provide the necessary background with a chronology of Talos’ success with its Zama discoveries, of which the latest appraisal well, Zama-3, was completed this past June.

He highlighted the historical breakthroughs made by Talos in the Mexican context, which have included the most core samples extracted (over 440m) and the first block unification agreement with PEMEX in Mexico’s history.

The historical dimension of these milestones promoted a transparent relationship with regulators and authorities that he believes plays a key role in their current and future success. “Talos wants to have a positive impact in Mexico. The president has set his production goal and we aim to do our part to help,” Noyola said.

“The success of MARINSA as a driller is to be committed to the objective of increasing production to contribute significantly to what Pemex and the Government of Mexico have established”

The panel then progressed toward the perspective of another private player whose successes have also been quite public as of late: Marinsa, represented by Chief Strategy Officer Sergio Suarez. After detailing the ways in which the crisis period during 2016 and 2017 prepared them for the road ahead, Suárez said that “The development of Marinsa has been the strengthened result of a set of readjustments to meet the needs of the national market and hill mentioning that Mexico has “qualified, strong Mexican suppliers and “under the conditions established by the current administration, being a national player gives us a competitive advantage. However, we also have strong alliances with international companies. ”

The CNH has had to experience “logarithmic learning” in order to perform its functions as a regulator, now it could reach response times for approvals as low as 34 days on average

Fausto Álvarez Hernández, Head of the Exploration and Production Compliance Unit at CNH, provided a direct public sector assessment of the success factors for offshore projects looking for a quick launch procedure.

He noted that CNH has had to experience “logarithmic learning” in order to perform its duties as a regulator as effectively as possible. He also praised the efficient path forward forged by ENI, Hokchi and Fieldwood toward first oil and eventual full production, which might total up to 220Mb/d from all three. “Optimization has been a key priority for CNH, particularly in approvals, as well as simplification in the documentation needed to present a project,” he said.

He also made a point of specifying that CNH now could reach turnaround times for approvals as low as 34 days on average, which he considers an extremely important component of fast offshore development.

Transparency and a long-term vision are key to sustainable social development projects. Enviromental Resources Management (ERM)

The fourth and final participant in the panel was Alberto Sambartolomé, Senior Partner at ERM, which has participated significantly in the sustainability assessments of many of Mexico’s offshore production projects. He highlighted the chief importance of efficiently introducing new operators to the legal and social expectations of the Mexican environment.

This not only leads to reduced downtime for drilling and development through quick regulatory compliance, but it also ensures the longevity of production once first oil is reached.

Projects that engage with regulators and communities early and promptly can look forward to productivity uninterrupted by protests or shutdowns, he said. “Transparency and a long-term vision are key for sustainable social development projects.”

Our country has a historic opportunity to demonstrate the competitiveness of the sector and recover its place in the world as an oil country without losing its vision of social development and environmental responsibility, thus concluded Graciela Alvarez Hoth this applauded panel.

https://nrgibroker.com/wp-content/uploads/2019/07/portadas-video-youtube_2.jpg10001000Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2019-07-26 16:20:162019-07-29 15:53:24Offshore Project Development: The Road to First Oil

The proposed US Mexico Canada Agreement (USMCA) makes important, but incomplete, progress in securing an integrated North American energy market.

In terms of progress, the agreement preserves zero tariffs for trade in oil, gas and petroleum products across North America. It effectively locks in Mexico’s historic energy reforms by ensuring that Mexico cannot reinstate restrictions on US investment in the oil and gas sector. A “ratchet” clause ensures that if Mexico decides to further liberalize the sector, then that higher floor becomes the new USMCA commitment.

While Investor-state dispute settlement (ISDS) mechanisms are weaker, they remain in force for certain “covered sectors,” including oil and gas investments in Mexico and power generation and pipeline investments where the investor has a contract with the government.

These are all positive steps for North American energy security. Mexico and Canada provide the United States with the heavy grades of oil not produced domestically, helping US refineries produce gasoline at the lowest possible cost. Thanks to this relationship, the United States is an efficient net exporter of petroleum products.

However, while this progress is laudable, it remains incomplete.

In the rush to conclude the agreement, effective protection for power generation investments like new wind and solar plants, refining and natural gas infrastructure, and power transmission lines were left out, perhaps inadvertently. Contracts for these investments are with state owned enterprises (SOEs) like Mexico’s CFE and PEMEX, which do not now fall within the definition of “federal government” because they are not disposing of assets but signing a contract for service. These essential investments, in the gas and refined product infrastructure which carry US products to and through Mexico, transmission lines which carry US electricity south, and investments in power generation are not permitted to bring ISDS claims to enforce their rights.

This is an oversight, and a protection these investments should enjoy. Rather, the proposed agreement creates an uneven playing field as investors who do have a contract with the Federal government, say for exploration, are entitled to bring an ISDS claim for any of their businesses, while those who do not have such contract do not. The problem can be easily fixed by expanding the definition of federal government to include these wholly owned SOEs.

These (for now) unprotected investments are critical to North American energy security. They secure US exports of electricity and natural gas and assure the continued reliability of the North American electricity system. They are the lifelines which carry US exports to Mexico – currently our number one customer for natural gas and petroleum products.

Protecting investments in Mexico’s electricity sector improves US national security by supporting Mexico’s prosperity through a more resilient power system.

Finally, if US power sector investments in Mexico are not protected and thus potentially hindered or lost, China is certain to fill the gap.

Chinese investment in all forms of power generation, transmission, and distribution is rapidly accelerating throughout Latin America. According to a recent Atlantic Council report, cumulative flows of Chinese foreign direct investment in Latin America have reached $110 billion, with $25 billion in oil and gas investment, and $13 billion in electricity, utilities and alternative energy. China’s State Grid has invested $7 billion in Brazil, through a combination of greenfield investments and acquisitions.

If the Mexican government is willing to offer these investments protections (and they are), and create a level playing field for American companies investing in our closest neighbor, the US should not object.

Fortunately, there is still time to correct the definition of eligible claimants as both sides ready the agreement for ratification. With these modest steps, the United States, Mexico and Canada can improve the resilience of North America’s energy system, and the US can simultaneously advance its economic and national security interests.

David L. Goldwyn is president of Goldwyn Global Strategies, an international energy advisory consultancy and serves as chairman of the Atlantic Council GlobalEnergy Center Energy Advisory Group. He served as the U.S. State Department’s special envoy and coordinator for international energy affairs from 2009 to 2011; he previously served as assistant secretary of energy for international affairs and as national security deputy to U.S. Ambassador to the United Nations Bill Richardson. He is a member of the U.S. National Petroleum Council and the Council on Foreign Relations.

https://nrgibroker.com/wp-content/uploads/2018/10/Putting-the-final-touches-on-the-USMCA.png400600Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-10-30 17:20:122018-10-30 17:21:02Unfinished business: Putting the final touches on the USMCA

Las garantías financieras son instrumentos a través de los cuales los titulares de los contratos firmados con la Comisión Nacional de Hidrocarburos (CNH), garantizan el cumplimiento de las obligaciones asumidas. Entre éstas se encuentran los seguros.

Su principal característica es la de fungir como un respaldo económico ante diversas contingencias, ya sea que recaigan en el mismo asegurado o un tercero afectado, como consecuencia de una acción u omisión del asegurado

Existen ciertas actividades en las que existe una mayor exposición al riesgo y con ello una mayor probabilidad de causar daños a terceros y en estos casos, las autoridades en aras de promover el bienestar general, incluyeron en las regulaciones los seguros para que los responsables cuenten con los recursos necesarios para reparar los daños o perjuicios ocasionados.

Es el caso de los seguros para el sector hidrocarburos que fueron regulados por la Agencia de Seguridad, Energía y Ambiente (ASEA) a partir de la Reforma Energética.

El artículo 6, fracción I, inciso c, de la Ley de la ASEA, establece la facultad de dicha Agencia, para: “Regular el requerimiento de garantías o cualquier otro instrumento financiero necesario para que los Regulados cuenten con coberturas financieras contingentes frente a daños o perjuicios que se pudieran generar…”

Los seguros que se requieren en el sector energético son complejos, pues generalmente a través de ellos, se amparan los riesgos de las operaciones de exploración y extracción de hidrocarburos en aguas profundas; transporte de petróleo por barco; tendido de ductos; construcción y operación de terminales de almacenamiento, etc.

Para asegurar adecuadamente a una empresa es necesario conocer su experiencia, sus características, sus medidas de seguridad operativa e industrial, sus obligaciones contractuales y lo más importante, el tipo de riesgos a los que está expuesta, considerando que:

Los hidrocarburos y petrolíferos son actividades peligrosas por sus características de inflamabilidad y explosividad;

Se les considera actividades altamente riesgosas;

Conllevaninfraestructura de grandes dimensiones y con altos grados de inversión económica;

Se pueden encontrar en zonas social y ambientalmente vulnerables y

Están expuestas a las acciones u omisiones de contratistas, sub-contratistas y proveedores de servicio.

NRGI Broker ofrece asesoramiento profesional para la contratación de los programas integrales de seguros, con las coberturas que pueden contratarse en México, pero también cuenta con la capacidad para colocar coberturas en el mercado internacional de reaseguro, cuando se trata de “grandes riesgos”.

En México experimentamos la reconfiguración del sector energético, que dio lugar a una mayor participación de empresas del sector privado, nacional e internacional, así como nuevas obligaciones por lo que las empresas requieren que sus inversiones estén correctamente respaldadas y trabajar con proveedores ágiles, con costos y tiempos de respuesta eficientes y para la consecución de ese objetivo, por ello es fundamental la contratación de un corredor de seguros experimentado, especializado y confiable.

En NRGI Broker, contamos con la experiencia y la especialización en seguros para todas las actividades el sector energético que necesitas. Acércate a nosotros, con gusto te atenderemos.

https://nrgibroker.com/wp-content/uploads/2018/09/5beneficios.png19201080Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-10-02 11:08:522018-10-02 11:08:52LOS BENEFICIOS DE LOS SEGUROS EN EL SECTOR HIDROCARBUROS

Los estudios de Línea Base Ambiental (LBA) son estudios de tipo técnico especializados que son requeridos por la Agencia de Seguridad, Energía y Ambiente(ASEA) de la Secretaria de Medio Ambiente y Recursos Naturales (SEMARNAT) a los regulados del Sector Hidrocarburos para: determinar las condiciones ambientales en las que se encuentran los componentes ambientales de las áreas contractuales, así como la identificación y registro de daños preexistentes y daños ambientales.

La LBA es también un insumo importante para la elaboración de las Manifestaciones de Impacto Ambiental, a efecto de cumplir con lo dispuesto en el contrato celebrado entre la Comisión Nacional de Hidrocarburos (CNH) y los Regulados. Los objetivos principales para la realización de los estudios de LBA son:

Identificar y describir la infraestructura existente en el área contractual y su estado actual físico y operacional para identificar y evaluar los daños ambientales que hayan sido generados por esta, para el deslinde de responsabilidades.

Identificar y evaluar las condiciones ambientales en que se encuentran los ecosistemas y recursos naturales, existentes en el área contractual y zona de influencia, previo a la ejecución de las actividades del contrato.

Evaluar los daños y pasivos ambientales ocasionados por las actividades humanas o procesos naturales en la zona contractual y de influencia a efecto de deslindarse de las responsabilidades

En el artículo 27, párrafo séptimo de la Constitución Política de los Estados Unidos Mexicanos, se establece que las actividades de exploración y extracción del petróleo y demás hidrocarburos se realizarán mediante asignaciones a empresas productivas del Estado o a través de contratos con éstas o con particulares, por lo que la presentación de la LBA ante la ASEA se traduce en una obligación para estas entidades.

Para orientar la elaboración de los estudios de LBA la autoridad a puesto a disposición de los regulados dos guias: a) “Guía para la elaboración y presentación de la Línea Base Ambiental previo al inicio de las actividades de Exploración y Extracción de Hidrocarburos en Áreas Terrestres” y b) la “Guía para la elaboración y presentación de la línea base ambiental previo al inicio de las actividades marinas de exploración y extracción de hidrocarburos en aguas someras”.

Es sumamente importante para los regulados que pretenden el aprovechamiento de zonas contractuales, el identificar, evaluar y detallar de manera precisa los daños ambientales preexistentes a través de los estudios de LBA, ya que solo podrán eximir su responsabilidad ambiental respecto a dichos daños, siempre y cuando hayan sido registrados y manifestados en dichos estudios.

Considernado la relevancia que tienen los estudios de LBA para los regulados, en cuanto al deslinde de los pasivos ambientales y sociales preexistentes de las áreas contractuales, es fundamental que dimensionen la necesidad de que la elaboración de la LBA debe ser realizada por empresas o plataformas técnico-científicas de especialistas calificados y con capacidad demostrada para la realización de este tipo de estudios. El deslindarse de dichos pasivos a través de buenos estudios de LBA y no asumir ningun riesgo financiero, social, legal y ambiental, es uno se los mejores seguros para sostener la viabilidad de sus inversiones y no comprometer su reputación como empresa y regulado ante la eventualidad de que se generen contingencias ambientales.

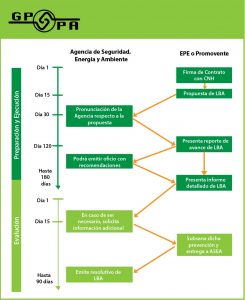

Un buen estudio de LBA debe sustentar además, las bases para el diseño e implementación de los Sistemas de Manejo y Gestión Ambiental y Social (SMGAS) para la prevención, manejo, mitigación y monitoreo de impactos ambientales y sociales durante las fases de preparación, construcción, operación y mantenimiento de los proyectos o de las áreas contractuales que deberán ser establecidos en las manifestaciones de impacto ambiental, estudios del cambio de uso del suelo de terrenos forestales, evaluaciones de impacto social y estudios de riesgo ambiental que correspondan. El proceso de elaboración y evaluación de los estudios de LBA se presenta en la siguiente figura:

Con más de 20 años de experiencia, cobertura internacional y fuerte compromiso con la sustentabilidad, la innovación y la calidad de nuestros servicios en el sector hidrocarburos, energía, turismo, desarrollo urbano, infraestructura, medio ambiente y minería; GPPA y nuestros socios estratégicos NRGI Brokers y Rodríguez Dávalos Abogados, asi como especialistas de diferentes institutos y centros de investigación, hemos conformado una plataforma técnico-cientifica de expertos nacionales e internacionales con la mayor capacidad en el país para ofrecer soluciones integrales y con valor agregado a los regulados del sector hidrocarburos, para resolver sus necesidades en materia de planeación, manejo, gestión ambiental y legal, desarrollo sostenible, fianzas y seguros de responsabilidad ambiental, incluyendo la elaboración de estudios de LBA, Evaluación de Impacto Ambiental, Evaluación de Impacto Social, entre otros productos y servicios.

Para mayor información y cualquier duda o necesidad derivada de la información presentada en el presente boletín, estamos a su disposición a través de:

Consultores en Gestión Política y Planificación Ambiental, S.C.

https://nrgibroker.com/wp-content/uploads/2018/09/WhatsApp-Image-2018-09-17-at-15.44.57.jpeg1043851Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-09-18 15:06:462018-09-18 15:06:46Línea Base Ambiental: Retos y Oportunidades para el Sector Hidrocarburos

The General Administrative Provisions that establish the Guidelines on Industrial and Operational Safety and Environmental Protection to carry out the activities of Surface Recognition and Exploration, Exploration and Extraction of Hydrocarbons (DACG/E&E), were published in the Official Gazette of the Federation, issued by the National Agency for Industrial Safety and Environmental Protection of the Hydrocarbons Sector (ASEA), established that those who carry out works or activities for the exploration and extraction of hydrocarbons are subject to a regime of strict liability, that is, they operate under the assumption that they are creating a risk to people and the environment and, therefore, in case of causing damage they must carry out its repair, without this being conditioned to prove their fault.

Derived from the above, ASEA imposes on operators the obligation to perform all actions necessary to prevent environmental damage arising from the risks created, for which they must contain, characterize and remedy them with opportunity under their own processes and according to the applicable legislation and regulations.

In this sense, the “DACG/E&E” establish that Exploration and Extraction activities must be carried out under certain principles, such as:

Minimize the risks at a level that is as low as reasonably possible, that is, up to a level where it is demonstrated that the cost of continuing to reduce that risk is greater compared to the economic benefit that would be obtained. This allows a reasonable balance between economic activity and the protection of third parties and the environment.

Regularly review the risk reduction measures in order to update them based on the technological development and specialized knowledge.

Implement emergency measures and foster a culture of the protection of people, the environment and facilities.

The aforementioned principles are aimed at preventing the accidents from happening, so they must be complemented with measures that have as their object the repair and / or compensation of the damages caused by the an accident.

One of the most effective measures to achieve this is to have financial instruments that allow for the consequences of the materialization of risks, such as an insurance.

At NRGI Broker we are experts in insurance for the Exploration and Extraction of Hydrocarbons. Come to us.

https://nrgibroker.com/wp-content/uploads/2018/09/El-régimen-de-responsabilidad-objetiva-en-las-actividades-de-Exploración-y-Extracción-de-hidrocarburos-1-1.png400600Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-09-11 12:37:362018-09-18 15:43:51The regime of strict liability in the activities of Exploration and Extraction of hydrocarbons

The Five-Year Expansion Plan of the National Integrated Natural Gas Transportation and Storage System 2015-2019 contemplates the construction of more than 5,000 km of natural gas pipelines, with an estimated investment of close to 10,000 million dollars. For its elaboration, the National Infrastructure Program 2014-2018 was taken as a basis, in which the gas pipeline construction projects are planned, with an approach that seeks to guide the integral functionality of the new infrastructure of the country.

On the other hand, the main objective of the Quinquennial Plan is to bring natural gas, considered the most efficient fuel and of intensive use, to different areas of the country, among which are Hidalgo, Puebla, Veracruz, Aguascalientes, Durango, Michoacán, Guerrero, San Luis Potosi, Chihuahua, Sonora, Oaxaca, Tamaulipas and Nuevo Leon, especially in industrial areas and those where up to now this hydrocarbon has not been accessed.

The foregoing is in line with one of the objectives of the Energy Reform, consisting of the safe, reliable and competitive supply of natural gas.

These new gas pipelines will be added to the more than 10,000 km already existing, and will increase the capacity of transportation of natural gas by 50%.

It is worth mentioning that the expansion of the gas pipeline network can bring with it a greater possibility of accidents, considering that the pipelines are one of the means of transport that present a greater frequency and severity of accidents, due to the fact that they are exposed to various hazards as: explosion, fire, natural phenomena and ill-intentioned acts.

Therefore, it is very important that during the construction and operation of the pipelines, the insurance coverage is adequate for the complexity of this means of transport, for which it must be taken into account that the damages may affect the infrastructure, people, their assets and the environment.

In NRGI Broker we are experts in designing comprehensive insurance schemes for the Hydrocarbons Sector, come to us.

https://nrgibroker.com/wp-content/uploads/2018/09/Captura-de-pantalla-2018-09-04-a-las-11.34.46-e1536079045279.png337600Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-09-04 11:48:542018-09-04 11:48:54The strategic value of the pipelines

A risk, according to the Law of the National Agency for Industrial Safety and Environmental Protection of the Hydrocarbons Sector (ASEA), is the probability that an undesired event will occur, measured in terms of its consequences to personnel, to the population, to facilities and equipment and the environment. In short, a risk is the probability of an accident occurring.

In this regard, it is important to consider that “risk” is not synonym to “danger”, since the latter refers to the intrinsic conditions or characteristics of an object capable of causing harm, while the risk is the probability of that damage occurring. From the above it follows that there are situations and objects that are dangerous themselves and therefore have the potential to cause harm, that is, they represent a risk, which however can be controlled and minimized.

In terms of hydrocarbons, oil and gas are hazardous materials, given their explosive and flammable characteristics. Therefore, the activities in which they are involved represent a risk, hence they are legally defined as highly risky activities.

In addition to the intrinsic characteristics, the operations carried out throughout the hydrocarbon value chain are highly complex, since 1) they involve large-scale infrastructure: drilling platforms, ship-tanks, pipelines, storage terminals, others; 2) are carried out in conditions that may be extreme, for example, drilling an oil well in the sea or traveling long distances through a ship or a train; 3) Advanced technology and specialized personnel are required.

Derived from the above, it is necessary to take all the measures in risk management to avoid accidents from happening. However, although a risk can be prevented and controlled, it can not be eliminated completely, so in any case, it will be necessary to transfer it, with the aim of preventing a company from absorbing the total economic losses that a loss may represent and that they can translate into a significant patrimonial detriment.

A risk can be transferred to an insurance company, through an insurance contract in which the insurer is committed to the insured, who in return for a premium, will indemnify him in case he suffers a loss that causes losses economic, as long as the event corresponds to the insured object, conforms to the terms and conditions established in the policy and is not an exclusion.

In the SectorHydrocarbons Sector, there are specific insurances to cover the risks inherent to this activity, which have also been established as mandatory by the regulatory authority (ASEA), such as: 1) Well control; 2) Civil Liability and 3) Environmental Responsibility.

At NRGI Broker, we are experts in insurance for the Hydrocarbons Sector. Come to us.

https://nrgibroker.com/wp-content/uploads/2018/08/Los-riesgos-en-el-Sector-Hidrocarburos.png400600Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-08-28 13:21:232018-08-28 14:01:51Risks in the Hydrocarbons Sector

La “Reforma Energética”de 2013 significó una apertura al sector privadoen esferas antes reservadas exclusivamente a órganos gubernamentales, tales como los sectores de infraestructura, hidrocarburos y energía; propiciando un modelo estratégico en el que los inversionistas pueden ser participantes en el desarrollo de proyectos de estos rubros como Empresas Productivas del Estado (EPE).

Estas EPE cuentan con personalidad jurídica y patrimonio propios, así como cierta autonomía que las empresas paraestatales y empresas públicas carecen; otorgando la posibilidad de abrir los sectores señalados con anterioridad a un panorama competitivo en el mercado mexicano. Con este nuevo paradigma, las prospectivas de los sectores eléctrico, de hidrocarburos y de energías renovables se amplían, como lo demuestran las siguientes cifras dentro de los documentos emitidos por la Secretaría de Energía (Prospectivas 2017-2031):

La producción estimada de aceite (miles de barriles diarios) aumenta de 1,964 a 3,252 al año 2031.

En el 2016, la capacidad instalada del Sistema Eléctrico Nacional se ubicó en 73,510 MW; pronosticando que para el 2031, esta cifra aumente hasta 113,269 MW.

En el 2016, existía un balance en el que la Energía Convencional comprendía un 71.2% y la Energía Limpia un 28.8% de la capacidad instalada por tipo de tecnología; previendo para el 2031 que la Energía Convencional ocupe un 50.4% y la Energía Limpia un 49.6%.

El incremento esperado de procesamiento de crudo es de 79.6% para el periodo 2017-2031.

Estos son ejemplos de las altas expectativas que se tienen del crecimiento en cuanto a producción, desarrollo y consumo de Energía e Hidrocarburos en poco más de una década. Con lo anterior en consideración, se debe prever que Empresas Productivas del Estado podrán realizar las siguientes actividades encaminadas a alcanzar estos Pronósticos:

Sector Hidrocarburos:Exploración superficial marítima y sísmica terrestre; Exploración y Extracción de hidrocarburos; Tratamiento y Refinación de Petróleo; Transporte de Hidrocarburos, Petrolíferos y Petroquímicos; Almacenamiento de Hidrocarburos, Petrolíferos y Petroquímicos; Distribución de Gas Natural y Petrolíferos; Compresión, licuefacción, descompresión y regasificación de Gas Natural; y Expendio al público de Gas Natural y Petrolíferos.

Sector Electricidad:Generación de Energía Eléctrica y Servicio público de transmisión y distribución de energía eléctrica.

En este tenor, es importante mencionar que la realización de todas estas actividades requerirán de la presentación de un estudio técnico denominado Evaluación de Impacto Social (EVIS), el cual contiene la identificación de las comunidades y pueblos ubicados en el área de influencia de un proyecto, así como la identificación, caracterización, predicción y valoración de las consecuencias a la población que podrían derivarse del mismo y las medidas de mitigación y planes de gestión social correspondientes.

En congruencia con lo establecido en la Ley de la Industria Eléctrica (LIE) y la Ley de Hidrocarburos, el 01 de junio de 2018, se publicó en el Diario Oficial de la Federación el Acuerdo por el que se emiten las Disposiciones Administrativas de Carácter General sobre la Evaluación de Impacto Social en el Sector Energético(el “Acuerdo”).

Dentro de este Acuerdo, se establece la metodología y criterios necesarios para la presentación del EVIS, un avance para la calidad de estos estudios por motivos de que la regulación y los lineamientos necesarios para la su elaboración eran escasos y no existían lineamientos definidos que pudieran usarse como base para las Empresas Productivas del Estado.

Finalmente, no se debe perder de vista la estrecha relación existente entre la Evaluación de Impacto Social y la Evaluación de Impacto Ambiental (EIA), en el entendido que la primera es un prerrequisito para la autorización de la EIA. Es requisito para los regulados contar en forma previa con las autorizaciones de ambos estudios para el desarrollo de los proyectos encaminados a los sectores de Energía e Hidrocarburos. En la siguiente figura se muestra el proceso de elaboración y evaluación de las EVIS.

Con más de 20 años de experiencia, cobertura internacional y fuerte compromiso con la sustentabilidad, la innovación y la calidad de nuestros servicios en el sector hidrocarburos, energía, turismo, desarrollo urbano, infraestructura, medio ambiente y minería; hemos conformado un catálogo de productos y servicios con valor agregado que resuelva en forma sistémica las necesidades de nuestros clientes y grupos de interés, en materia de planeación, manejo, gestión ambiental y desarrollo sostenible, incluyendo la elaboración de EVIS y la EIA. Para ello, ponemos a su disposición la red más amplia y especializada de expertos a nivel nacional e internacional, ofreciendo una plataforma integral en la materia, trazando las alternativas y estrategias necesarias para el correcto desarrollo de Proyectos Sustentables en México, entre ellos.

Para mayor información y cualquier duda o necesidad derivada de la información presentada en el presente boletín, estamos a su disposición a través de:

Consultores en Gestión Política y Planificación Ambiental, S.C.

On July 27, Mexican president-elect Andrés Manuel López Obrador said his government will earmark more than $9 billion for state-run energy companies next year and start working on a new oil refinery in southern Mexico. The moves seek to reduce reliance on fuel imports from the United States while boosting the country’s oil production, which has significantly fallen off in recent years. López Obrador did not say how he would fund his proposals, an omission that worries analysts concerned about Pemex’s already heavy debt burden. He also announced Octavio Romero Oropeza as the incoming head of Pemex. Will the promised investment help accelerate Pemex’s oil and gas production? What else is needed to boost output? How well prepared is Romero Oropeza to lead Pemex, and what should his priorities be? Four Mexican energy experts weighed in with their opinions on these developments.

George Baker, publisher of Mexico Energy Intelligence in Houston: The 116-page energy sector document that the Morena transition team issued on July 10 sports both good and bad ideas. First, among the good ideas, is advocating independent unions in the oil sector (the first time since 1935 that a political party has done this). Second is suspending until further review the so-called farm-outs of Pemex—the idea that civil servants (Pemex employees) and market-disciplined managers of oil companies can have a joint venture based on sharing risk and reward only makes sense on paper. Third is promoting the concept of intelligent cities, including low energy consumption, renewable energy and intelligent grids. A fourth good idea is expanding the grid of natural gas pipelines and the use of renewable energy sources and cogeneration. Among the bad ideas: first is reactivating the refinery project in Tula and analyzing the construction of another refinery in the Gulf of Mexico. Pemex refinery upgrades have gone badly for the past 20 years, notably in Cadereyta, Villahermosa and Tula. A new refinery could take three years just for design and another three for contracting and financing. López Obrador would likely leave office before the first shovelful of earth was turned for the new refinery. Second is the upgrade of the role of Pemex in the energy space. The Morena team proposes to eliminate the so-called ‘asymmetrical regulations’ that restrict Pemex to compete effectively—to aspire to ‘make Pemex great again’ as a state agency is to ignore global success stories of state oil companies with mixed-equity structures, market financing and professional management. Finally, a third bad idea is to overstate (and obfuscate) the potential for change via public policy: there is nothing that is actionable in statements such as ‘the necessary investments in Pemex should be made,’ or ‘efforts to increase exploration and production of natural gas should be made to favor the petrochemical industry,’ or ‘deepen and coordinate all efforts to eliminate the black market in petroleum products.’ Notably, one word that does not appear in the text is ‘corruption,’ an unexpected omission by a candidate that vowed to end corruption by example. Finally, former Pemex director general Adrián Lajous recently calculated the average tenure of a director general as two years and four months. Pemex, legally configured as an agency of the federal government, always has a dozen cooks in its kitchen of corporate governance. If a director general had the authority to order early retirement for 35,000 Pemex unionized workers, there would be opportunities for leadership.

David Shields, independent energy consultant based in Mexico City: In a previous comment for the Energy Advisor on June 15, I mentioned that President-elect López Obrador’s energy team has excellent, progressive plans in renewable energy. Sadly, the same does not apply to conventional energy. The naming of Octavio Romero and Manuel Bartlett to head state-run Pemex and the Federal Electricity Commission (CFE) has been severely criticized because of their hardline political, ideological, non-technical, non-business nature. They may be okay for rooting out corruption, but they add to fears that recent energy reforms may be rolled back, even if they and López Obrador himself deny legal amendments will be made. Congress will ultimately decide on this, and the outlook there is bad. Reforms can be reversed in practice, anyway, just through day-to-day opposition. López Obrador says he will push oil output up sharply to 2.5 million barrels per day, but reserves and reservoirs are largely depleted, there are no new discoveries, and there is not enough money for a vast exploration effort. Foreign operators will need several years to develop their projects. His best bet for ramping up output quickly would be fracking, but he promises to prohibit that, thinking that environmental risks will be greater than the benefits. His refining plans are unrealistic, too. López Obrador´s native Tabasco State offers the wrong site and the wrong logistics for a large-scale refinery to be built in just three years. Such a project normally requires two years to study, plan and tender, then another five or six years to build. Even then, it can hardly be profitable if Mexico produces and processes only very heavy crude. Intentions to rescue Pemex and reduce reliance on energy imports are good, but the prospects are not.

https://nrgibroker.com/wp-content/uploads/2017/12/pemex-e1528826043964.jpg397600Soportehttps://nrgibroker.com/wp-content/uploads/2023/08/nrgibroker-300x96.pngSoporte2018-08-21 16:59:452018-08-21 17:00:30Is Mexico Set To Boost Oil Output?